Marketplace rates for children will rise 20% to 53%, on top of the additional average 42% rate increase insurers in Ohio demand in 2018.

Child rates in the past they have always been 63.5% of the adult base rate until the age of 21. Next year, 0-14 will be 76.5% of the adult base rate, with ages 15 to 20 being 83.3% to 97% of the adult base rate.

2018. Individuals, those who don’t get health insurance from an employer or from the government, are supposed to feel lucky to at least still be able to buy health insurance. We were warned that rates would go through the roof this year. That’s due to the uncertainty of the government reimbursing insurers for CSRs, the uncertainty over the insurance requirement mandate, the uncertainty of a repeal, as well as the totally understandable (not), predictable, ever-rising, unsustainable, runaway medical and non-negotiable pharmaceutical cost factors, that alone amount to a 7% rate increase in 2018, along with the resumption of the ACA tax on premiums that was halted last year, and some increases in administration costs. We braced for rates going up 40% or more.

On top of the outrageous, unbelievable rate hikes for adults that are 40 times the rate of inflation going to our little sector of the healthcare business, CMS snuck in that equally as outrageous and unbelievable rate hike for children.

A typical family may see a rate hike of 29% for themselves, and 71% for their children.Typical family, photographed here in 2000, has been through it all

A Little Story About A Typical Family

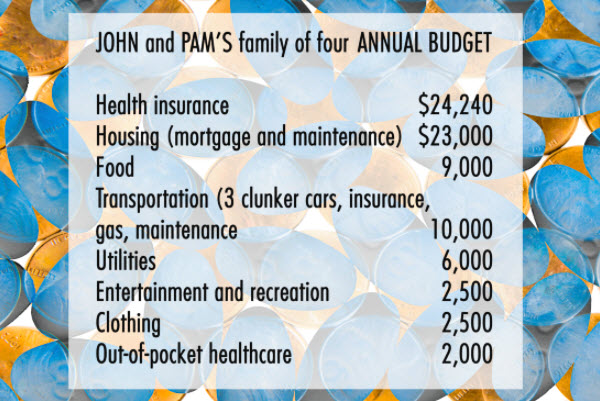

Take your typical Ohio family – say, John and Pam, who are 55. They have two kids who are 17 and 20. John is an independent contractor and earns $78,000. Pam is an adjunct university professor and earns $21,000. Together they make $99,000 before taxes, just over the 400% Federal Poverty Level that would qualify them for a health insurance subsidy. Their net income after taxes is $78,000.

Having to buy individual insurance, they chose Molina, because that was the only plan in which they could find doctors who would accept them as patients.

Toledo, Ohio is a closed town when it comes to doctors accepting new patients. When it became too costly in 2016, John and Pam had to give up their Medical Mutual PPO insurance and hence their ProMedica doctors that they had been going to for 20 years. Molina was one of the cheapest insurance plans they could buy. But they had to find new doctors, because their long-time doctors didn’t accept Molina insurance.

MercyHealth doctors are in the Molina network, and they are not as closed as ProMedica doctors. That’s why our typical family chose Molina over CareSource, another cheap plan, but one with a 90% inaccurate provider network, a network that supposedly included ProMedica doctors, but not really. (ProMedica, when last checked, had only one primary care family practice doctor accepting new patients, but you’d have to call back in a month to schedule an appointment, which supposedly would be scheduled for three months after that.*)

If John and Pam had made just two thousand dollars less (see Kaiser subsidy calculator here), this typical family would have qualified for a $3,334 subsidy this year (undoubtably it would be more than $6,000 in 2018 because the SLCSP which is tied to the subsidy may be 20-30% more, in tandem with the rest of the plans; see rate increases below.) The subsidy would have reduced their health insurance premiums to 10% of their gross income for a silver plan, but alas, they make too much money to qualify.

John and Pam chose a gold plan with a lower deductible because they couldn’t afford the risk, just in case, of having to come up with $7,500+ to meet the deductible before the insurance would kick in.

With an increase of over $6,000 in 2018 for health insurance, their tightest budget, cutting down on food, recreation, transportation and clothing, exceeds their net income. Forget about helping with their kids’ education or even saving for their own retirement, which is coming in 10 short years – in 2018, they will be going into credit card debt on their necessary expenses just to be able pay for health insurance.

As it was, in 2016 John and Pam paid 22% of their net income on health insurance, $17,448, at $1,454/month (John and Pam’s rates were $554.50 each per month, and the kids’ rates were $172.62 each). It was considerably more than they were paying just a few years before. An affordable and reasonable percentage as written in the ACA would be 13% of their take-home, or 10% of their gross. 22% of their take-home pay on health insurance made their budget very tight.

Next year, John and Pam’s health insurance will go up 39%. Health insurance will surpass housing as biggest chunk of their budget, becoming a whopping 31% of their take-home income, $24,240 for the year; $2,040/month. The astronomical but necessary expense for health insurance squeezes out any money that could ever have been saved for retirement, which they need to fund, and eliminates any possible budget they may have hoped for to help their kids with higher education expenses.

While John and Pam’s health insurance is going up 29%, health insurance for their kids goes up 71%. The family’s health insurance premiums next year will cost $6,792 more than last year!

Too bad for the 30% of the individual market, like John and Pam, who don’t get a subsidy; their health insurance expense is simply unsustainable. They may have to keep working into their seventies, because there’s no way they can save money for retirement when the insurer gets every red cent. And their kids can forget about college.

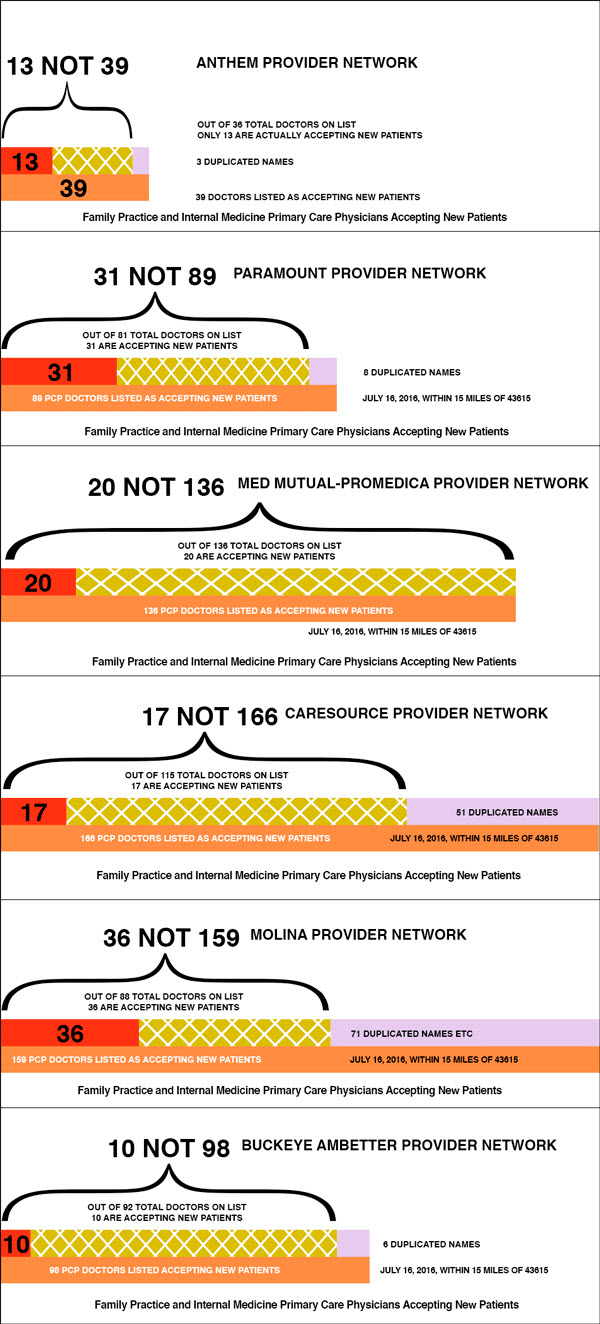

This survey was made in July and August 2016 of all the internal medicine and family practice primary care doctors listed on the networks of healthcare.gov plans offered by Anthem, Paramount, Med Mutual-Promedica, CareSource, Molina, and Buckeye Ambetter within 15 miles of 43615, Toledo, Lucas County, Ohio. On each provider network directory connected to the plans on healthcare.gov, I searched for internal medicine and family practice primary care doctors who are accepting new patients. I compiled a list of all the doctors listed as accepting new patients, totaling 308.* I called their offices and asked if they were accepting new patients.

:To Recap

Anthem Blue Cross Blue Shield has 13, not 39 PCP family practice and internal medicine doctors accepting new patients. 67% inaccurate.

Paramount has 31, not 89 PCP family practice and internal medicine doctors accepting new patients. 65% inaccurate.

Med-Mutual-ProMedica has 20, not 136 PCP family practice and internal medicine doctors accepting new patients. 85% inaccurate.

CareSource has 17, not 166 PCP family practice and internal medicine doctors accepting new patients. 90% inaccurate.

Molina has 36, not 159 PCP family practice and internal medicine doctors accepting new patients.77% inaccurate.

Buckeye Ambetter has 10, not 98 PCP family practice and internal medicine doctors accepting new patients. 90% inaccurate.

The average of the six percentages representing the inaccuracies, misrepresentations, falsely advertised lies, untruthfulness and phoniness in our Toledo provider network databases is EIGHTY PERCENT !!

Here are some things I was told by the doctors offices.

Seven said they keep calling to have the list changed but they don’t update, one moved to Arizona, one moved to California, one moved to Oak Harbor, one moved to Bowling Green three years ago, two are retired, one isn’t practicing anymore, six you must pay an additional annual membership fee of $1,650 and they still take your insurance, five are geriatrics only, two more only see patients in the nursing home, one more only sees patients in Hospice, two only see mental health patients, five said they have no control over the lists, one only sees Owens Corning employees and asked twice to be taken off the list, eight screen for age, address, state of health and doctors you’ve seen and then decide if they are accepting new patients or not, 15 do not accept new patients but their residents do, 26 do not accept new patients but their nurse practitioners do, one is not practicing medicine anymore, two are not PCPs, one only sees addiction program patients, eight are hospitalists, one is a hematologist, one is a sleep doctor, five are kidney doctors, not PCPs, one sees only adolescents, one is a pediatrician, three are sports doctors, six were not locatable, more than one said they put doctors on the list without asking and they never update them, one said they haven’t accepted new patients for 30 years, etc., etc., etc….

Ironically, Lucas County has one of the highest resident to PCP ratios in the entire state of Ohio, so why is it that the overwhelming majority of PCP doctors are not taking new patients? Are they being extinguished by insurance companies by not being paid enough money, useful in name only for the time being, to populate provider network directories that lead to nowhere in an Orwellian scheme that ?controls utilization and increases corporate wealth, or what?

The Skinny on Narrow Networks in Health Insurance Marketplace Plans is a study made by the Robert Wood Foundation. It quantifies what makes a small or extra small network. Toledo has maybe 450 primary care physicians. An extra-small network has 11% or less of the total number of physicians practicing in an area. That would be about 50 PCPs in Toledo. A small network has 30% or less, which for Toledo would be about 135 PCPs. The insurers are lying about the doctors’ availability to make their networks seem larger. Doctors that don’t accept new patients and haven’t for years can hardly be considered in-network for new patients. From my survey, which shows 13 to 36 PCPs available in the network to new patients, not even one of those is of a sufficient sized network to be allowed to sell on the Marketplace.

Excerpt from CMS’s 2017 letter to Issuers:

What will the CMS do about Toledo’s grossly inaccurate provider databases?

R.I.P. American Dream. If you are an artist, writer, musician, inventor, entrepreneur, shop owner, lawyer, plumber, carpenter, waitress, or any number of hard working workers with jobs that don’t provide large group employer-based health insurance, quit right now and run for cover! It’s survival time! This year, thanks to the uncertainties, the calculated congressional and presidential threats, and the other garbage that politicians have thrown at us all year long, health insurance premiums are 42% higher for adults, and 60% to 85% higher for the kids. Even newborn babies are being welcomed to the world by a big, double-digit rate hike. Surprise!

Furthermore, while prices have risen 500% in the past five years for individuals, national network PPOs have been eliminated for individuals. Individuals are left with Medicaid-like health maintenance organizations, which are considerably less health insurance than the PPO plans that Ohio got rid of last year. I’m sorry for the artists, writers, musicians, inventors, entrepreneurs, shop owners, etc. Did you ever think that having health insurance would be such a huge obstacle in your quest for success?

R.I.P. PPOs., the last bastion of equal healthcare along side the big corporation counterparts. It isn’t fair.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.Accept

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.